![]()

020 3982 0420

![]()

We're incredibly proud of our achievements over the years, not least because we have received such great testimonials and continue to grow, even in the face of confusing NHS reimbursement changes. Here's why we think you should look at Practice Cover for your locum insurance.

The opinions presented in this blog are solely those of the author on behalf of Practice Cover Limited and they do not constitute individual advice. Practice Cover is a trading name of Practice Cover Limited and is authorised and regulated by the Financial Conduct Authority

Earlier this year when the new GMS contract was announced many thought it was the end of locum insurance. To be honest, it panicked us, because we’re the only company in the UK that focuses 100% on locum insurance.

We could hear GPs’ thoughts. “Why would my practice need to buy insurance when the NHS would provide something similar?”

The measures announced in the contract were designed to improve the financial position of GP practices – a good thing. In most part the measures were costed. For example, £156.7m has been set aside to cover for the discontinuance of AUA DES; £30m for indemnity insurance costs; and so on.

But we asked the question, “where are the sickness absence reimbursement figures?”, because we can see that no cost has ever been publicly attributed to what was announced as a significant change in sickness cover reimbursement for GPs.

We’ve been talking to you. GPs are struggling to see where the funding is coming from. We are already hearing that some CCGs and health boards have a set amount of money, most already spent, and some GPs are finding it difficult to claim under their GMS contract.

While we fell into a cold sweat with the GMS announcement, the facts have surprised us. GPs still recognise the need for locum insurance. They see the NHS sickness reimbursement as something of a lottery – not a statistical certainty.

Here’s what’s happened to us. We can announce our best ever year of trading since we started out. The number of GP cases is 27% up and premium income is 14% up (ytd 2017 vs 2016)

Of course we also provide locum insurance to other healthcare professionals, and the number of cases is 30% up and premium income is 19% up.

We think it’s because our policies provide some certainty. For a relatively low premium practices have the chance to receive a payment from their locum insurance policy alongside the NHS reimbursement payment. For example, if a GP is insured for a monthly premium of £120pm the practice could receive £2500pm PLUS any claim made under your GMS contract.

We’re also very open about our service and our premiums. We haven’t increased our rates in almost 8 years, against a landscape of premium rises across the insurance sector. Transparency is a good thing to us. You know where you stand – and we have a very loyal customer base because of it.

Not insured yet? Well, the secret of getting ahead is getting started*. Click here to get a locum insurance quote.

* With apologies to Mark Twain for borrowing his quotes.

All figures are as at end October 2017.

** Cover for a full-time GP would cost around £120 pm (after tax relief) and, for this, the practice would receive £2,500 pw for up to 52 weeks (after a 4 week waiting period) in the event of a valid claim.

The opinions presented in this blog are solely those of the author on behalf of Practice Cover Limited and they do not constitute individual advice. Practice Cover is a trading name of Practice Cover Limited and is authorised and regulated by the Financial Conduct Authority

I was listening to radio 4’s ‘You and Yours’ and they were talking about NHS funding of IVF.

I was listening to radio 4’s ‘You and Yours’ and they were talking about NHS funding of IVF.

The issue was around the NICE guidelines* which say that women over 40 should be allowed 3 cycles of treatment and that this is at odds with what is happening in reality. It appears that the dreaded ‘postcode lottery’ comes into play and, in some CCG areas you’d be lucky to get one cycle, never mind 3.

Their interviewee – a GP and Chief Clinical Officer at a CCG – said that, notwithstanding the NICE guidelines, they had ‘difficult decisions’ to make as regards utilising the ‘set amount of money’ they have been allocated, they had to ‘prioritise’, and CCGs had to take into account ‘their financial position’.

As a locum insurance provider, this makes my alarm bells ring. In February 2017 a number of measures were announced to improve the financial position of GP practices and, in most part, the measures were costed: £156.7m to cover for the discontinuance of AUA DES, £30m for indemnity insurance costs, and so on.

One of the measures to which, as far as I can ascertain, no cost has ever been publicly attributed was a significant change in sickness cover reimbursement for GPs.

This was followed by speculation that this had killed off the need for locum insurance.

In the months that have followed we’ve seen that many GP practices have taken the NHS announcement with a pinch of salt. I have lost count of the number of GPs and practice managers who have told me they can’t see where the funding is coming from, they don’t think it will last, they will have to fight to get the money to which they are entitled and that, essentially, handing over their insurance to the NHS could be a very bad move.

In my view the NHS provision should be a safety net for those GPs whose health renders them either uninsurable or for whom locum insurance may be punitively expensive.

If your practice is in an area where ‘difficult decisions’ need to be made and your CCG has only a ‘set amount of money’ which it has already spent it is not inconceivable that obstacles will be put in your way if you try to claim under your GMS contract for GP sickness absence.

In fact we have already had reports from GPs and practice managers of this happening.

So, what price can you put on that type of lottery? Locum insurance doesn’t come with such uncertainty. Cover for a full-time GP would cost around £120 pm (after tax relief) and, for this, the practice would receive £2,500 pw for up to 52 weeks (after a 4 week waiting period) in the event of a valid claim.

In the event of receiving a payment from the NHS, your locum insurance will not be affected – potentially a win-win for the practice.

If you’d like to know more, please call me.

Lynda Cox

The opinions presented in this blog are solely those of the author on behalf of Practice Cover Limited and they do not constitute individual advice. Practice Cover is a trading name of Practice Cover Limited and is authorised and regulated by the Financial Conduct Authority

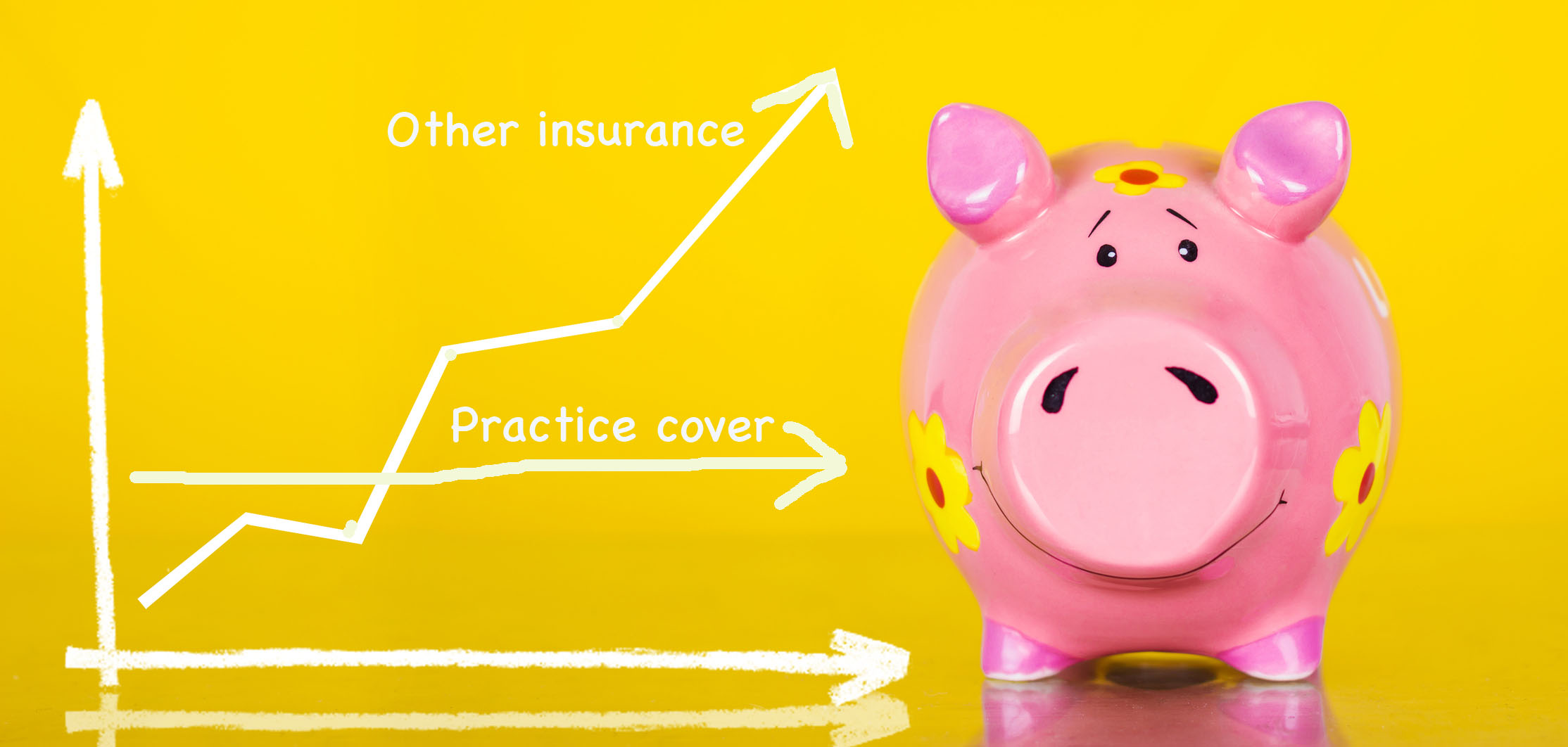

Across the insurance sector premiums have been rising. It affects all of us and is a bitter pill to swallow when we haven’t made claims, pay on time and even show loyalty. Let’s look at some recent examples.

Comprehensive motor insurance premiums are up 19.6% on average over the past 12 months – and 8.3% in the last quarter according to the AA**. Third party, fire and theft premiums are up a whopping 24.7% year on year. The damage looks to be less when you look at home insurance premiums, with buildings up 2.4% and contents 3% over the last 12 months, but the trend is upwards.

Doctors, dentists, opticians and the like are not immune to the pain of these premium increases. All the more important, then, that you should find some solace in your locum and overheads insurance premiums.

The good news is that Practice Cover has not increased its clients' premium rates... ever! Why? It’s because we value loyalty, and offer what we feel is the best insurance at the right price. While we can’t absorb tax increases – and sadly the rate of Insurance Premium Tax rose again in June – we have not touched our premium rates.

Our competitors are making price increases, and in a sector where insurers are paying out £9.9m every day* on protection policies this may not sound surprising.

But we have no plan to follow suit. Just look at the facts on how we’re adding value at every stage:

· At Practice Cover even clients who have made a claim have not been charged a higher premium. That’s not how we work.

· We have a ‘continuity of cover’ option with our locum insurance so that, if you become ill – let’s say you have a heart attack – the underwriters won’t exclude heart attacks from your future cover.

· We include a no claims discount so premiums can actually reduce by staying with us.

· We can confirm that premium rates will stay the same in the foreseeable future – as they have for more than 7 years.

These facts explain why we’re one of the most stable and cost-effective providers of locum insurance and overheads insurance on the market.

If you’d like to know more about our policies, then speak to Lynda Cox on 0800 028 5633.

* Insurers’ pay outs for protection policies, including income protection, critical illness and life insurance. Source ABI 2017.

** AA British Insurance Premium Index Q2 2017

The opinions presented in this blog are solely those of the author on behalf of Practice Cover Limited and they do not constitute individual advice. Practice Cover is a trading name of Practice Cover Limited and is authorised and regulated by the Financial Conduct Authority

Most GP practice managers have enough on their plates without having to perform acrobatics.

Let’s assume one of your GPs is off sick and you’re pretty sure you can claim the cost of covering for him/her from your CCG (or LHB, if you're in Wales).

Does your CCG/LHB tell you to jump through hoops?

If so, this might help …

Hoop 1: they tell you to provide a copy of the partnership agreement to show 'who's responsible' for meeting the cost of sickness absence.

Your response should be: 'responsibility' is irrelevant. If a GP performer at a GMS or PMS practice goes off sick the practice is entitled to claim from the CCG/LHB once he or she has been off for 2 weeks.

Hoop 2: they tell you to provide invoices for external locums to support the amount claimed.

Your response should be: cover doesn't have to be provided by external locums. Practices are eligible for reimbursement if the practice's existing doctors cover - as long as those doctors are not full-time.

Hoop 3: they tell you that, as you've got a locum insurance policy, you can't claim reimbursement.

Your response should be: whether a practice has locum insurance in place or not is irrelevant. Practices are eligible for reimbursement if a GP performer is off sick for more than 2 weeks. Any locum insurance payment that a practice receives should not be taken into account.

For help jumping through hoops call Practice Cover on 023 8051 3286.

The opinions presented in this blog are solely those of the author on behalf of Practice Cover Limited and they do not constitute individual advice. Practice Cover is a trading name of Practice Cover Limited and is authorised and regulated by the Financial Conduct Authority

Changes made to the GMS contract in April have left many GPs and practice managers wondering just what protection they have if there’s a key absence through sickness or accident in the practice.

In this article we’ll look at two scenarios involving nurse practitioners, because the sickness absence funding under the GMS contract will not apply in either circumstance.

Many practices are utilising the skills of certain primary care practitioners, such as a nurses, paramedics and pharmacists as the front line and, alongside key staff like practice managers, their absence from work can leave a huge hole in daily clinical provision.

However, sickness absence funding from the NHS is only available for GP performers. If it’s not a GP that’s absent then there is no right to this type of reimbursement for the practice.

Locum insurance from Practice Cover, however, can be taken out to protect against sickness and absence of key staff. There’s also no restriction on how you use funds from a claim to cover the absence, which brings us on to our second point.

If the absence is that of a GP performer, then the guidance is relatively clear. Non-discretionary reimbursement is available to the practice. For more about how much you can claim through sickness absence funding under the GMS contract please email This email address is being protected from spambots. You need JavaScript enabled to view it. and ask for a PDF copy of our GP reimbursement leaflet.

The crucial point is that the NHS will only reimburse against your claim if you use a GP to provide cover. Many practices will utilise the skills available within the practice to cover for a GP’s absence, such as a nurse practitioner. However the new provisions do not allow for the cost of this. Practices can claim only if cover is provided by either locum GPs or by GPs who are already working part-time at the practice.

Formally: "The commissioner will not pay for cover provided by nurses or other healthcare professionals" (from NHSE document "Protocol in respect of locum cover or GP performer payments for parental and sickness leave").

So while is makes good sense to use the non-GP resources available to you, you’re not covered for this.

Again, it may be prudent to ‘top up’ your NHS provision with locum insurance cover. Any claim made under our locum insurance can be spent in the way you wish – so you could fund extra sessions for nurses as you see fit.

If you’re confused about the rules around sickness absence funding under the GMS contract, then speak to Lynda Cox on 0800 028 5633.

The opinions presented in this blog are solely those of the author on behalf of Practice Cover Limited and they do not constitute individual advice. Practice Cover is a trading name of Practice Cover Limited and is authorised and regulated by the Financial Conduct Authority

Many thanks for your prompt service.

Practice Cover limited registered in England (no 7063423) Authorised and regulated by the Financial Conduct Authority. Correspondence address: Practice Cover Ltd, Devonshire Business Centre, Works Road, Letchworth SG6 1GJ

Registered office address: 255 Green Lanes, Palmers Green, London N13 4XE

The information contained in this website is subject to the UK regulatory regime and is therefore restricted to consumers based in the UK.

Website by The Oxygen Agency Ltd